Car damage does not always happen in traffic accidents involving other drivers. Many drivers damage their own cars in everyday situations. A garage wall, a curb, a parking barrier, or a fallen branch can cause expensive repairs in seconds.

These incidents often create confusion. Drivers expect insurance to help, but coverage does not always apply. Auto insurance in the United States is regulated at the state level, and coverage depends on the type of policy selected, not on the situation alone.

Insurance policies are built around defined risks. Some cover crashes. Others cover events unrelated to driving. Many drivers only carry the minimum required coverage and assume it protects their own vehicle. That assumption often leads to unexpected repair bills.

Understanding coverage before damage happens changes outcomes. It helps drivers choose the right protection, avoid denied claims, and plan financially. It also prevents stress during an already frustrating moment.

This guide explains how auto insurance treats damage to your own car. It covers collision coverage, comprehensive coverage, liability limits, deductibles, claim decisions, and rate impacts.

Does Insurance Cover Damaging My Own Car?

Damage to your own vehicle is covered only with collision or comprehensive coverage. Collision protection applies to crashes and rollovers, while comprehensive coverage applies to theft, weather damage, and falling objects. Liability coverage does not apply.

Insurance coverage for personal vehicle damage depends entirely on the structure of the policy. Fault does not determine whether coverage applies in single vehicle incidents. What matters is how the damage occurred and which coverage types are active.

You can protect your vehicle from unexpected repair costs by carrying the right auto insurance coverage for collision and non collision damage.

Collision coverage applies when a vehicle is damaged due to physical impact. This includes hitting a pole, a wall, a curb, or another stationary object. It also applies if the vehicle overturns, regardless of road conditions or driver behavior.

Even when no other driver is involved, collision coverage treats the event as a covered loss if the policy includes it.

Comprehensive coverage applies to damage that happens without a driving impact. These events include theft, vandalism, fire, hail, floods, falling trees, and animal collisions.

Comprehensive coverage focuses on unpredictable events that occur outside normal driving scenarios. For example, a tree falling on a parked car or hail damaging the roof would fall under comprehensive coverage.

Liability insurance works differently. It exists to protect other people, not the policyholder’s vehicle. Liability pays for injuries or property damage caused to others.

To make coverage differences easier to understand, it helps to compare how each insurance type responds to damage. This side by side view shows which policies protect your car, which protect others, and what the law requires.

| Coverage Type | Covers Your Car | Covers Others | Required by Law |

| Collision | Yes | No | No |

| Comprehensive | Yes | No | No |

| Liability | No | Yes | Yes |

It does not pay for repairs to the insured car under any circumstance. Drivers who carry only liability coverage must pay for their own repairs when they damage their own vehicle.

Deductibles also play a role in how much insurance pays. Both collision and comprehensive coverage include deductibles. The deductible is the amount paid by the policyholder before insurance contributes.

If repair costs are lower than the deductible, insurance provides no payment. This makes deductible selection an important part of coverage planning.

Understanding these distinctions prevents confusion during claims. Insurance responds according to the type of coverage in place and how the event is classified.

Drivers who understand this structure can choose policies that reflect real risks instead of assumptions, reducing financial surprises when damage occurs.

How Collision Coverage Works in the US

Collision coverage pays for damage to your car caused by impact, such as hitting another vehicle, a wall, a pole, or the road during a rollover. It applies to single vehicle accidents and covers repairs after crashes regardless of fault or road conditions.

Impact related damage is covered when a vehicle collides with another car, a stationary object, or the ground in a rollover, including single vehicle accidents.

Single vehicle accidents fall under collision coverage even when no other car is involved. Weather conditions, road hazards, or sudden obstacles do not change how the damage is classified under the policy.

According to the North Dakota Insurance Department, collision coverage applies when a vehicle is damaged by impact, regardless of who is at fault.

Collision coverage includes a deductible. The policyholder must pay this amount before insurance contributes toward repair costs. If damage costs less than the deductible, insurance does not provide payment.

Lenders often require collision coverage for financed or leased vehicles. Once the loan is paid in full, this coverage becomes optional and is often reevaluated based on vehicle value.

Collision claims are commonly treated as at fault incidents. Because of this, filing a collision claim can affect future insurance premiums depending on insurer rules and claim history.

How Comprehensive Coverage Works in the US

Comprehensive coverage pays for damage to your car caused by non collision events such as theft, fire, vandalism, weather, falling objects, or wildlife contact. It applies when damage occurs without a driving impact and includes a deductible defined in the policy.

This coverage applies when vehicle damage is not caused by a collision while driving and is designed to protect against losses that occur outside normal traffic accidents. These events are often sudden and unavoidable.

Covered incidents include theft, fire, vandalism, hail, floods, falling trees, and contact with wildlife. Damage may occur while the vehicle is parked, moving, or unattended. The defining factor is that no collision caused the damage.

The North Carolina Department of Insurance notes that comprehensive coverage, also known as other than collision, pays for damage caused by falling objects, fire, theft, windstorm, hail, flood, vandalism, riot, or contact with wildlife.

The official Massachusetts insurance website states that comprehensive coverage applies to loss or damage caused by events other than a collision, including vandalism, fire, theft, falling objects, and animal contact.

The Oregon Division of Financial Regulation reports that comprehensive coverage typically covers damage from fire, theft, explosion, glass breakage, animal collision, and other events not included under collision coverage.

Animal related damage is consistently classified as comprehensive coverage across U.S. state insurance authorities. This includes contact with deer or other wildlife, regardless of whether the vehicle was moving.

Weather related damage is one of the most common comprehensive claims. Hailstorms, floods, and wind driven debris can damage vehicles quickly and without warning. These events occur outside driver control.

Falling objects also fall under comprehensive coverage. Tree limbs, construction materials, or damaged structures can strike a vehicle without any driving action involved. These losses are treated as comprehensive claims.

Comprehensive coverage includes a deductible that must be paid before insurance contributes to repairs. Deductibles for comprehensive coverage are often lower than collision deductibles, depending on the policy.

Insurance policy terms can be complex and easy to misunderstand. Working with a qualified insurance agent helps confirm comprehensive coverage, deductible details, and how protection applies to your vehicle.

If repair costs fall below the deductible, insurance does not provide payment. Choosing an appropriate deductible helps balance premium cost and financial risk.

Comprehensive claims generally have less impact on insurance rates than collision claims. Insurers view these events as external and not caused by driver behavior.

State insurance laws do not require comprehensive coverage, but lenders often mandate it for financed or leased vehicles to protect against unpredictable losses.

The Legal Information Institute at Cornell Law School presents comprehensive insurance as coverage for most vehicle damage that does not occur in a collision, including hail, theft, vandalism, and falling tree limbs.

Understanding comprehensive coverage helps drivers plan for risks that careful driving alone cannot prevent. It provides protection against environmental and criminal events that can damage a vehicle at any time.

To fully understand how coverage applies, it helps to compare comprehensive protection with collision coverage and see how each responds to different types of damage. This comparison also makes it clear where coverage ends, which leads directly into what liability insurance does not cover.

What Liability Coverage Does Not Pay For

Liability insurance does not pay for damage to your own car. It only covers injuries or property damage you cause to others. Repairs to the insured vehicle, towing, or replacement costs are excluded under liability coverage in all situations.

Liability insurance exists to protect other people from financial loss caused by a driver. It does not exist to repair or replace the policyholder’s own vehicle. This distinction is central to how auto insurance works in the United States.

Liability coverage is divided into two main parts. Bodily injury liability pays for medical expenses, lost wages, and related costs when others are injured. Property damage liability pays for damage to someone else’s vehicle or property.

Neither part of liability coverage applies to the insured vehicle. If a driver damages their own car by hitting an object, liability insurance provides no payment for repairs. The policyholder is responsible for all costs.

This limitation applies regardless of fault or circumstances. Single vehicle accidents, parking incidents, and weather related driving damage are not covered under liability insurance. Coverage depends on policy type, not the situation.

The California Department of Insurance clearly states that liability coverage does not pay for damage to the policyholder’s vehicle. It is designed only to compensate others for losses caused by the insured driver.

Many drivers misunderstand this limitation because liability coverage is required by law. State insurance laws focus on protecting the public, not protecting the driver’s own property. Meeting legal requirements does not guarantee vehicle protection.

Drivers who carry only liability coverage face full financial responsibility for repairs to their own vehicle. This includes body damage, mechanical damage, and total loss situations. Insurance does not contribute in any amount.

This misunderstanding often surfaces after a first single vehicle accident. Drivers expect insurance to help because premiums are paid regularly. The denial feels unexpected but follows policy terms exactly.

Liability coverage also does not pay for theft, vandalism, fire, or weather damage. These losses fall outside its scope entirely. Only comprehensive coverage applies to those situations.

Understanding what liability coverage excludes is critical when choosing an insurance policy. Drivers who want protection for their own vehicle must add collision or comprehensive coverage to their policy.

Without those coverages, any damage to the insured car becomes an out of pocket expense. This includes repairs, rental costs, and vehicle replacement.

Recognizing these exclusions makes it easier to understand how different types of coverage respond to different events. With that foundation clear, it becomes helpful to examine common damage scenarios and which coverage applies in each case.

Common Insurance Damage Scenarios

Coverage depends on how car damage occurs. Collision applies to impacts like hitting objects or rollovers. Comprehensive applies to non collision events such as weather, theft, falling objects, or animal contact.

Different incidents trigger different types of coverage under U.S. auto insurance policies. Insurance companies classify claims based on the event that caused the damage. This classification determines whether collision or comprehensive coverage applies.

Hitting a pole, wall, or barrier is considered a collision event. Even if the vehicle was moving slowly or parked incorrectly, the damage resulted from impact. Collision coverage applies in these situations when included in the policy.

Scraping a garage wall or damaging a car while parking also falls under collision coverage. The vehicle made contact with a fixed object. The absence of another driver does not change the classification.

Rollovers are also treated as collision claims. Even when caused by road conditions or obstacles, the vehicle impacts the ground. Collision coverage applies to these losses.

Damage caused by falling objects follows a different rule. A tree falling on a parked car is not considered a collision because the vehicle did not strike anything. Comprehensive coverage applies in this case.

Weather related damage is another common scenario. Hail damage, flood damage, and wind driven debris are all classified as comprehensive losses. These events occur without driver action.

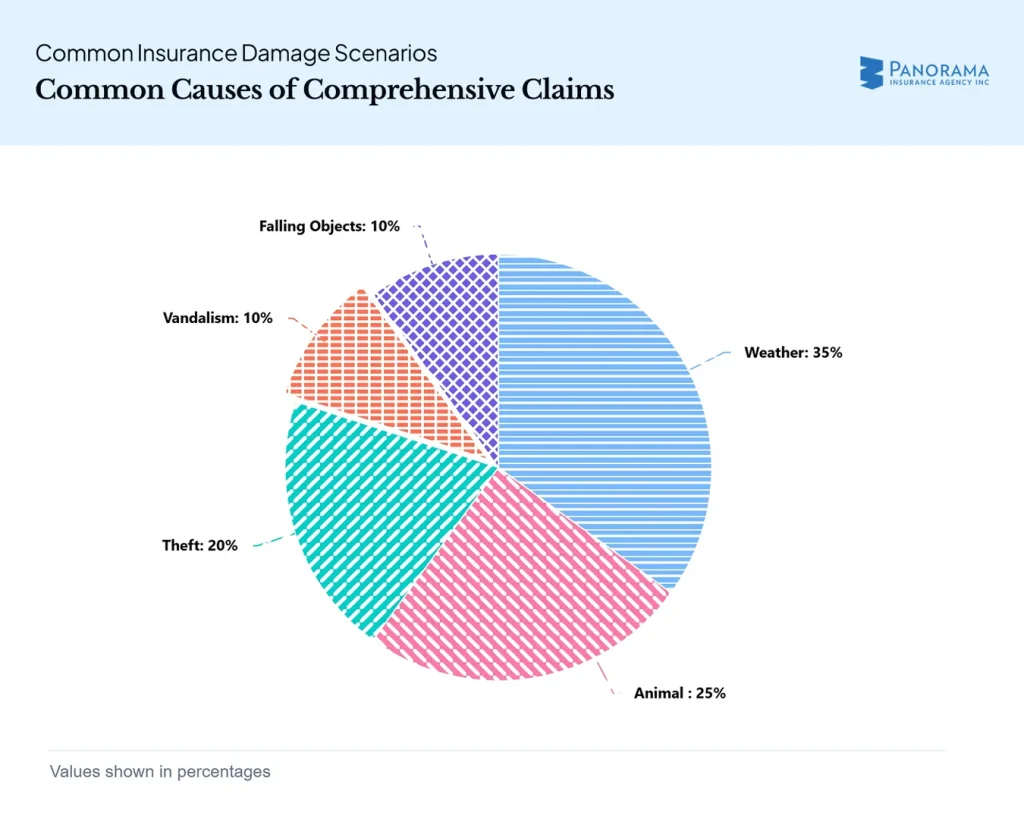

This pie chart shows the most common causes of comprehensive insurance claims. Weather accounts for 35%, animal collisions 25%, theft 20%, while vandalism and falling objects each represent 10%.

Animal contact is also treated as comprehensive coverage. Collisions with deer or other wildlife are not classified as collision claims under U.S. insurance standards. This distinction often surprises drivers.

Vandalism and theft are always handled under comprehensive coverage. Broken windows, key scratches, or stolen vehicles fall outside collision coverage entirely.

Fire damage follows the same rule. Whether caused by an electrical issue or external source, fire damage is handled as a comprehensive claim.

Insurance companies focus on the cause of loss rather than where it happened. A car damaged in a driveway is evaluated the same way as one damaged on a highway. Location does not affect coverage classification.

Intent also does not determine coverage. Accidental damage triggers coverage if the correct policy applies. Intentional damage is excluded under all coverage types.

Understanding these scenarios helps prevent claim confusion. Drivers often expect coverage based on circumstances rather than classification. Insurance policies apply strictly defined rules.

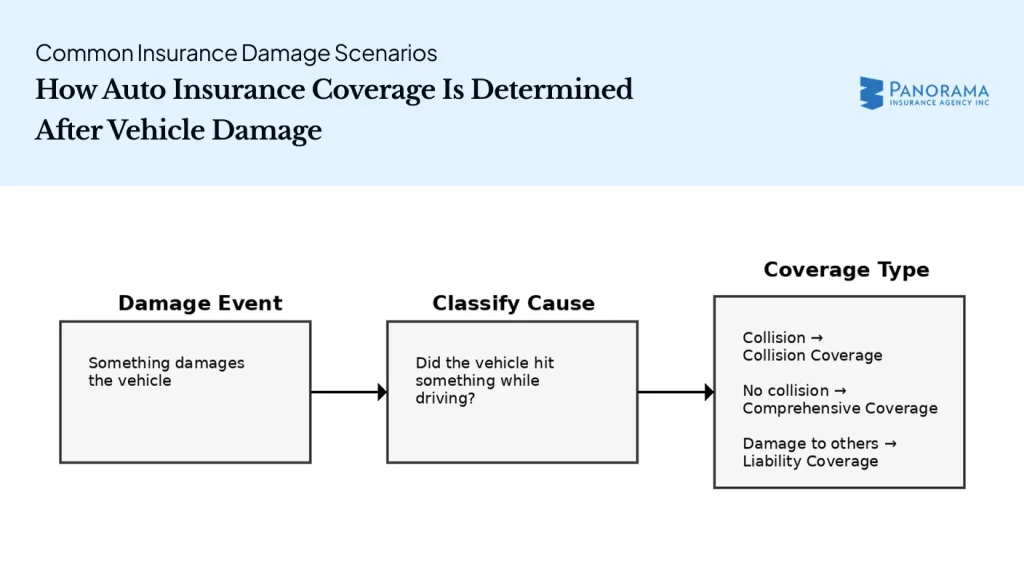

This flow diagram explains how auto insurance coverage is determined after a damage event. Insurers first need to identify whether the vehicle was involved in a collision, then assign collision, comprehensive, or liability coverage based on how the damage occurred.

To clarify how this decision process works in real situations, the table below summarizes common damage scenarios and the type of coverage that applies.

| Situation | Coverage Type |

| Hit a pole | Collision |

| Scraped garage wall | Collision |

| Tree falls on parked car | Comprehensive |

| Hail damage | Comprehensive |

| Animal collision | Comprehensive |

This breakdown shows how coverage applies consistently across situations. Similar damage outcomes may be covered differently depending on cause.

Knowing how insurers classify damage helps drivers choose appropriate coverage. It also helps set expectations before filing a claim.

Once coverage type is identified, the next factor that determines actual payout is the deductible. Understanding deductibles explains how much insurance pays versus what the policyholder must cover out of pocket.

Insurance Deductibles and Out of Pocket Costs

Deductibles are the amount paid before insurance applies, while out of pocket costs include expenses insurance does not cover. If repairs cost less than the deductible, insurance pays nothing and all costs remain the driver’s responsibility.

A deductible is the amount the policyholder must pay before insurance contributes to a covered repair. This amount is selected when the policy is purchased and applies each time a claim is filed.

If a deductible is set at five hundred dollars, the driver pays the first five hundred dollars of repair costs. Insurance only pays the remaining balance after that amount is met.

When repair costs are lower than the deductible, insurance does not provide payment. Filing a claim in this situation results in no reimbursement while still recording a claim.

Deductibles apply per claim, not per policy year. Multiple incidents during the same coverage period require the deductible to be paid each time.

Higher deductibles reduce monthly premiums because the driver accepts more financial responsibility. This option works best for drivers who can handle unexpected repair costs.

Lower deductibles increase premiums but reduce out of pocket expenses after damage. This provides more predictable costs when repairs are needed.

Policies may have separate deductibles for collision and comprehensive coverage. For example, comprehensive deductibles are often lower due to different risk patterns.

Out of pocket costs extend beyond deductibles. Rental vehicles, towing, storage fees, and uncovered repairs may still require personal payment.

Understanding deductible structure prevents surprise expenses after an accident. Many drivers focus on premium cost without fully considering repair responsibility.

Deductibles play a direct role in claim decisions. Knowing how much must be paid upfront helps determine whether insurance involvement is worthwhile.

With deductible responsibility clearly understood, the next step is deciding when filing a claim actually provides financial value and when paying for repairs personally makes more sense.

When Filing an Insurance Claim Makes Sense

Filing an insurance claim makes sense when repair costs clearly exceed the deductible or when damage affects safety or drivability. Claims should balance immediate repair needs against long term premium impact and uncovered out of pocket expenses.

A claim provides value when insurance payment meaningfully reduces repair costs. If damage exceeds the deductible by a wide margin, insurance absorbs most of the expense and limits financial strain.

Safety related damage should be repaired promptly. Issues affecting steering, braking, visibility, or structural integrity require attention regardless of potential premium changes.

Minor cosmetic damage often does not justify a claim. Scratches or dents near the deductible amount can result in no payment while still adding a claim to the policy record.

Out of pocket factors matter. Rental cars, towing, storage fees, and excluded repairs can reduce the benefit of filing even when coverage applies. If you are unsure how a claim may affect costs or coverage, get an expert opinion to determine the best course of action and avoid unnecessary expenses.

Claim frequency influences future pricing. Multiple claims signal higher risk to insurers, which can affect renewal costs over time.

Understanding when a claim provides value helps drivers avoid unnecessary costs. That evaluation becomes even more important when considering how much coverage makes sense based on the current value of the vehicle itself.

Choosing Coverage Based on Vehicle Value

Coverage should reflect vehicle value. Older cars with low market value often do not justify collision coverage, while newer vehicles with higher repair and replacement costs benefit from broader protection based on deductible size and financial risk.

Vehicle value is a core factor in insurance decisions. Insurance is meant to protect against financial loss, not restore value that no longer exists. As a car ages, the cost of coverage can exceed its benefit.

In the United States, the average age of passenger vehicles is over 12 years, according to the U.S. Bureau of Transportation Statistics. Older vehicles generally have lower market value and higher depreciation.

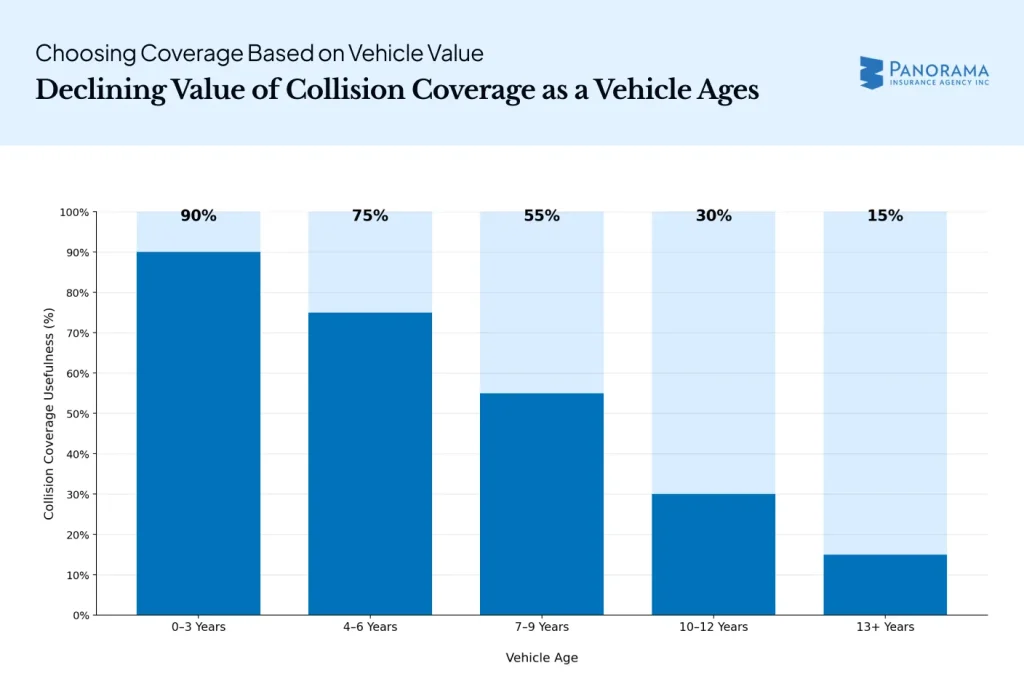

This chart shows how collision coverage usefulness drops as vehicles age, from about 90% for cars under 3 years old to 15% for vehicles over 13 years old. The decline reflects depreciation, repair costs, and deductibles reducing the value of coverage over time.

For an older vehicle worth three thousand dollars, collision coverage with a one thousand dollar deductible may provide limited value. After the deductible, insurance may pay only a small amount, if anything.

Newer vehicles face higher repair and replacement costs. Modern cars include advanced safety systems, sensors, and electronics. Repairs after even minor accidents can exceed several thousand dollars.

Deductibles directly affect payout. A high deductible reduces premium cost but increases out of pocket exposure. When deductible amounts approach vehicle value, coverage effectiveness drops sharply.

Replacement value also matters. If replacing the vehicle would cause financial strain, broader coverage offers protection against sudden loss. Insurance works best when coverage decisions are tied to clear numbers rather than habit.

Conclusion

In the United States, insurance pays for damage to your own car only if collision or comprehensive coverage is included. Collision covers impacts and rollovers, while comprehensive covers non collision events like theft or weather. Liability does not apply.

Understanding coverage types prevents confusion and financial strain. Clear knowledge allows drivers to choose protection that matches real world risks rather than assumptions.

Insurance decisions shape long term costs. Knowing what coverage applies ensures informed choices before damage occurs.