A traffic stop can create financial uncertainty, even when no ticket is issued. Many drivers leave the roadside with a warning and later question whether that interaction will affect their insurance premium.

The concern is understandable because auto insurance pricing is based on risk evaluation, and risk evaluation depends on recorded driving behavior.

Insurance companies calculate premiums using data pulled from official state motor vehicle records. These records document convictions, moving violations, points, accidents, and license status.

Each entry represents measurable risk. The more documented risk factors a driver has, the more the insurer adjusts pricing to reflect potential future claims.

Warnings create confusion because they involve law enforcement but do not always involve court action or fines.

Drivers often assume that any written document from an officer automatically enters the same system as a citation. Others believe insurers have access to police databases beyond the state driving record.

To evaluate whether a warning has financial consequences, it is necessary to understand how driving records are created, what insurers can legally access, and how underwriting decisions are made during policy renewals and new applications.

Will a Warning Raise Your Insurance?

A police warning by itself does not raise your insurance premium because insurers base rates on recorded violations and convictions shown on your official motor vehicle record. If no ticket is issued and no conviction appears, there is no pricing impact.

Insurance companies calculate premiums using verified state data. The primary document they review is your Motor Vehicle Record, known as an MVR. This report is issued by your state’s Department of Motor Vehicles and contains measurable driving events.

An MVR typically includes:

- Moving violation convictions

- Points assessed to your license

- At fault accidents

- License suspensions or revocations

- DUI or serious traffic offenses

It does not include informal roadside discussions. If an officer issues only a warning and no citation, there is no court case. Without a court case, there is no conviction. Without a conviction, nothing is added to the MVR.

Insurers usually review driving records at three key times:

- When you apply for a new policy

- At renewal periods

- After certain claim events

During underwriting review, companies use automated systems to scan for chargeable events. A warning without a recorded violation does not trigger those systems.

Warning vs Citation Comparison

The financial impact depends on how the stop is classified. The table below shows the structural differences insurers rely on during underwriting review.

| Factor | Warning | Citation |

| Fine issued | No | Yes |

| Court required | No | Yes or payable |

| Points added | No | Often |

| Appears on MVR | No | Yes |

| Impacts premium | No | Yes |

The difference is documentation. Insurance pricing depends on documented risk events. A citation creates a formal legal record. A warning does not.

Even written warnings, which may be stored in internal police systems, generally remain outside the state reporting structure used by insurers.

Insurance carriers do not access local police databases for informal warnings. They rely on standardized state reporting systems.

Rate increases occur only when underwriting guidelines identify chargeable activity. Examples include speeding convictions, reckless driving convictions, or at fault accident findings.

These events have statistical loss data behind them, which insurers use to calculate increased risk exposure.

If you want confirmation, request a copy of your MVR from your state DMV. Most states provide online access for a small fee. If the warning does not appear on that record, your insurer does not see it and cannot use it to adjust your rate.

The key principle is measurable risk. Insurers price based on recorded history, not warnings that carry no legal consequence. To see why that distinction matters, it is important to understand the specific data points insurance companies analyze during underwriting.

What Insurers Actually Review

Insurers review official state driving records, traffic convictions, license actions, and prior claims when setting premiums. They do not access or rate informal police warnings, only documented violations that appear on your motor vehicle record.

Insurance underwriting is data driven. Carriers request structured reports from state motor vehicle agencies and national claims databases. These systems contain legally recognized entries, not discretionary roadside actions.

The National Highway Traffic Safety Administration confirms that states maintain driver history files containing crash involvement and adjudicated violations. Those files feed into reporting systems insurers rely on.

Core Data Sources Used in Underwriting

Insurers typically assess the following categories:

1. Conviction History

- Moving violations finalized in court

- Reckless driving findings

- Driving under the influence convictions

- Failure to appear outcomes

2. Accident Records

- At fault determinations

- Property damage severity

- Bodily injury involvement

- Frequency of reported incidents

3. License Activity

- Suspensions

- Revocations

- Administrative penalties

- Compliance actions

4. Insurance Claim Databases

- Prior payout amounts

- Claim patterns

- Coverage gaps

- Policy cancellations

These categories contain measurable legal events. They exclude warnings that carry no adjudication.

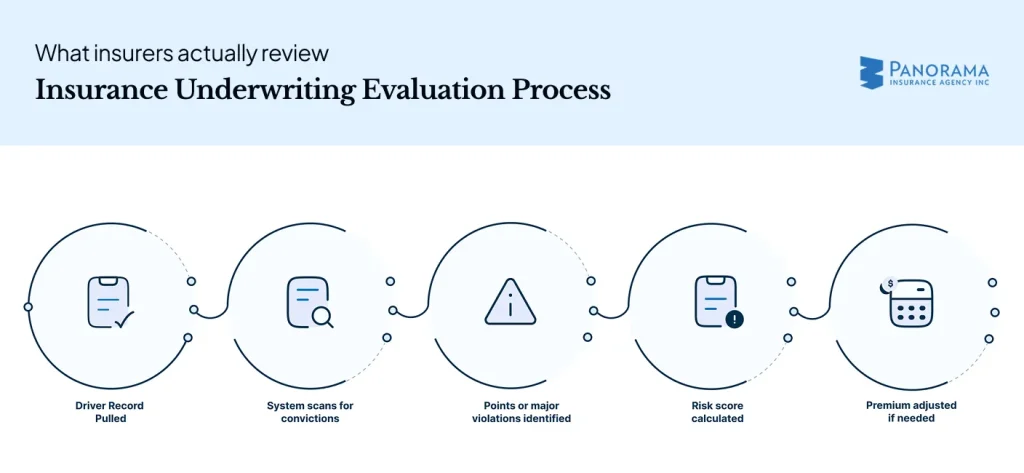

How Underwriting Evaluation Works

Once reports are obtained, insurers follow a structured review process. The evaluation is systematic and automated in most cases.

The process generally follows this structure demonstrated below:

The process above shows how insurance underwriting reviews driver records in a structured, automated way.

The system scans for convictions, assigns a risk score, and adjusts premiums if needed. If no conviction appears, no rate change occurs because insurers rely only on officially reported data.

What Typically Appears in State Records

State motor vehicle agencies maintain standardized records of legally processed driving events.

Only violations that move through the court or administrative system are formally entered into this database.

The table below shows common entries found on a state driving record and indicates which ones insurers use when calculating premiums.

| Entry Type | Court Adjudicated | Used for Rating |

| Minor speeding | Yes | Yes |

| Major speeding | Yes | Yes |

| DUI | Yes | Yes |

| At fault crash | Yes | Yes |

| Equipment violation | Yes if cited | Sometimes |

| Verbal warning | No | No |

| Written warning | No | No |

A violation becomes rate relevant only after it passes through the legal system and is recorded by the state.

Why Insurers Limit Their Review

Insurance pricing must follow regulatory standards. Carriers cannot use informal or unverifiable data to justify premium adjustments. State insurance departments oversee rating practices to ensure decisions are based on documented risk factors.

Underwriting models rely on statistical correlation. Convictions and crash history have measurable links to future claims. Internal police caution records do not provide standardized, statewide data and therefore cannot be rated consistently.

In short, insurers evaluate formal legal outcomes and documented claim behavior. If an event does not appear in the official state reporting structure, it does not enter the premium calculation process.

Review your record and discuss your policy with a reliable insurance agent to ensure your premium is based on accurate information.

Types of Traffic Warnings Drivers Receive

Police warnings are verbal or written notices issued without a ticket, court action, or license points. Because they do not create a recorded violation in state systems, insurers cannot access or use them when calculating auto insurance premiums.

Law enforcement officers use warnings as a compliance tool. They address minor driving behavior without initiating formal enforcement procedures. While both types acknowledge that a traffic rule was observed, they stop short of triggering administrative penalties.

The classification of the warning determines how it is handled internally by law enforcement, but neither form advances into court processing.

Verbal Warnings

A verbal warning is delivered orally during the traffic stop. The officer explains the observed issue and releases the driver without written documentation tied to a citation system.

There is no enforcement follow through beyond the stop itself. The interaction concludes without legal escalation.

Key attributes of a verbal warning include:

- No citation number generated

- No court filing created

- No administrative review initiated

- No transmission to statewide driver databases

Because the process ends immediately, there is no pathway into systems that influence insurance underwriting.

Written Warnings

A written warning includes documentation created by the officer at the scene. The driver may receive a copy noting the reason for the stop. However, this document is not a charging instrument.

It does not require a response, payment, or court appearance.

Core features of a written warning include:

- No financial penalty assessed

- No requirement to contest or resolve

- No judicial determination made

- No entry recorded as a violation

Written warnings are generally stored within local enforcement records for internal reference. They serve as documentation of officer discretion, not as a legal finding.

Structural Difference from Citations

To understand why warnings remain outside insurance review systems, it helps to compare their procedural path.

Below is a simplified process comparison showing how a citation progresses versus how a warning stops at the initial stage.

| Enforcement Action | Court Processing | State Record Entry | Insurance Visibility |

| Citation issued | Yes | Yes | Yes |

| Warning issued | No | No | No |

A citation activates a legal chain reaction. It proceeds through adjudication and is entered into state databases. A warning does not trigger that chain.

The absence of adjudication is the defining factor. Insurance pricing systems rely on standardized, court finalized events. Warnings remain discretionary enforcement actions without legal classification.

For drivers, the practical effect of a warning is instructional rather than financial. It signals observed conduct but does not create a documented violation within regulatory reporting systems.

The contrast becomes clearer when you look at the types of events that move beyond instruction and enter formal record systems. Those documented events are what insurers classify as chargeable and use to adjust premiums.

When Insurance Rates Go Up

Insurance rates rise after documented events like traffic convictions, at fault accidents, DUI offenses, or license suspensions. These are recorded in state systems and signal higher claim risk, which insurers use to recalculate and increase premiums.

Insurance pricing is based on measurable exposure. Carriers adjust premiums only after legally recognized events that indicate elevated future loss potential. These events are standardized, recorded, and statistically modeled.

The Insurance Information Institute confirms that traffic violations and accidents are primary rating factors used in auto underwriting.

Events That Commonly Trigger Rate Increases

Insurers typically raise premiums after one or more of the following:

- Moving violations that carry license points

- Multiple speeding convictions within a short period

- At fault collision claims

- Driving under the influence convictions

- Reckless driving findings

- License suspension or revocation

Each of these outcomes passes through a legal or administrative process. That process generates a permanent entry in statewide reporting systems.

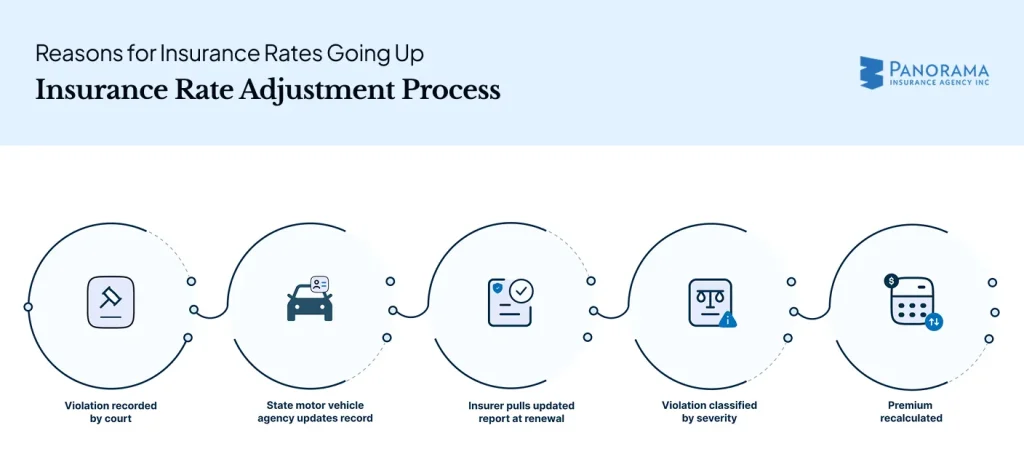

How Rate Adjustment Typically Happens

When a documented violation appears, the underwriting system follows a structured path:

The flowchart shows the structured path that leads to a premium change. After a court records a violation, the state updates the driving record. At renewal, the insurer reviews the report, classifies the violation by severity, and recalculates the premium if required.

The recalculation depends on severity and frequency. A minor speeding conviction may cause a moderate increase. A DUI conviction leads to substantial premium escalation because of its statistical link to high claim costs.

Why Documented Violations Matter

Insurance companies rely on actuarial science. Actuaries analyze historical loss data to determine how certain driving behaviors correlate with future claims.

For example:

- Drivers with multiple speeding convictions show higher collision frequency.

- Drivers with DUI convictions show significantly higher injury claim severity.

- Drivers with recent at fault accidents have elevated short term claim probability.

The Federal Highway Administration reports millions of traffic citations issued each year, demonstrating how common recorded violations are within national data systems.

These citations feed into state databases that insurers access during underwriting review.

Severity and Timing Influence Impact

Rate increases are not uniform. Several variables affect pricing:

- Number of violations

- Type of offense

- Time elapsed since conviction

- State specific rating regulations

- Insurance company underwriting guidelines

Most insurers apply a surcharge for a defined period, often three to five years, depending on the violation category. More serious offenses remain chargeable longer.

A single minor violation may cause a modest premium adjustment. Multiple violations within a short time frame create cumulative risk scoring, which results in higher increases.

The defining factor is official documentation. Premium adjustments occur only after measurable, adjudicated events enter the reporting system used by insurers.

Once a violation is recorded, the next critical factor is duration. How long that entry remains active in rating models determines how long it affects your premium.

Duration of Traffic Violations in Insurance Rating

Most minor traffic violations affect insurance rates for about three years from the conviction date, while major offenses like DUI can impact premiums for five to ten years, depending on state law and insurer guidelines.

Traffic violations remain on driving records for a defined period set by state law. The length of time depends on the severity of the offense. Minor infractions typically expire sooner than serious offenses.

In many states, minor moving violations stay on a driving record for three to five years. Major violations, such as reckless driving or DUI, remain longer because they indicate greater risk exposure.

Insurance companies apply their own rating windows within those legal timelines. Most insurers surcharge minor violations for approximately three years from the conviction date. More serious offenses may be rated for five years or longer.

Below is a general timeframe reference:

- Minor speeding: about 3 years

- Major speeding: up to 5 years

- At fault accident: about 3 years

- DUI conviction: 5 to 10 years depending on jurisdiction

The countdown usually begins on the conviction date, not the date of the traffic stop. If a driver contests a ticket and the court delays judgment, the rating clock starts only after final adjudication.

Once the violation ages beyond the insurer’s rating period, the surcharge is removed at renewal. The record may still exist in state archives, but it no longer affects pricing calculations.

A warning carries no rating duration because it never enters the conviction system. Without a recorded violation date, there is nothing to age and nothing to surcharge.

However, record retention rules and reporting structures are not identical nationwide. To fully understand how entries are stored and shared, it is important to look at how different states manage driving records.

State Driving Record Rules for Insurance

Driving record rules vary by state in how long violations stay on file and how points are assigned. However, across states, only court finalized violations and license actions are reported to DMV systems, while informal warnings are generally excluded.

Driver record management is regulated at the state level. There is no single national traffic record system used for auto insurance underwriting. Each state determines how records are stored, how long they are retained, and which events qualify for entry into the official database.

Although formats differ, the reporting standard follows a consistent rule. Only legally processed violations and administrative actions are entered into state motor vehicle records.

How States Manage Driving Records

State Departments of Motor Vehicles maintain centralized driver history files. These records are updated only after a court decision or formal administrative action.

Typical entries include:

- Final citation outcomes

- Traffic conviction records

- License suspensions or revocations

- Administrative penalties

- Verified crash reports

Written warnings may remain in local law enforcement systems for internal tracking. However, they do not move into the statewide DMV database because no adjudication occurs.

The National Highway Traffic Safety Administration explains that states maintain driver history files that include crash and conviction data.

How Insurers Access State Data

Insurance companies do not pull information directly from police departments. They request standardized motor vehicle reports from state agencies or authorized reporting providers.

Those reports contain:

- Conviction history

- License status

- Recorded suspensions

- Court processed violations

Events without court action are not transmitted into these reports.

Differences Between States

While all states report adjudicated violations, differences exist in:

- Record retention periods

- Point assignment structures

- Classification systems for minor versus major offenses

- Processing timelines

Some states use point based systems. Others classify violations by severity without assigning numerical points. Despite these structural differences, warnings remain outside the official reporting system because they are not court finalized.

The Federal Motor Carrier Safety Administration also confirms that driver record information is maintained at the state level.

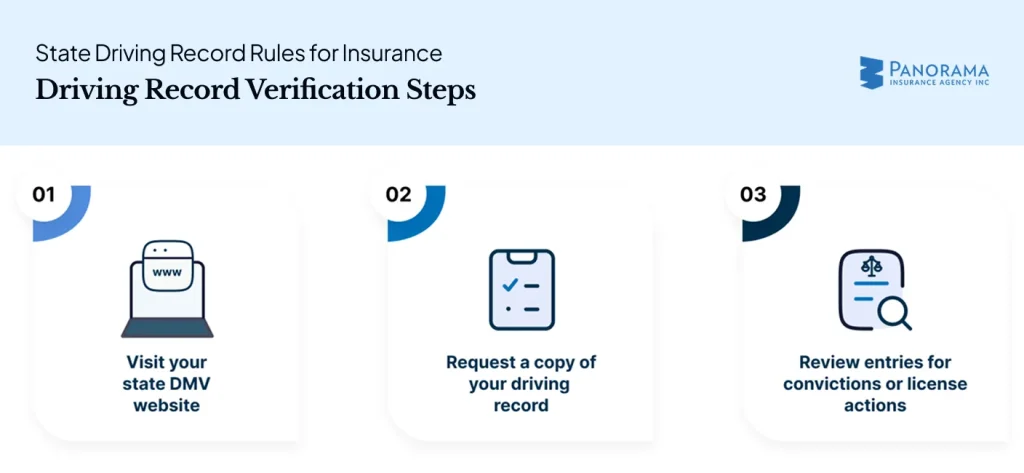

How to Confirm Your Own Record

Drivers can request a copy of their driving history directly from their state DMV. Most states offer online access for a small administrative fee.

The steps above outline how to verify your driving record. Visit your state Department of Motor Vehicles website, request a copy of your official driving record, and carefully review it for any listed convictions, points, or license actions that may affect your insurance rate.

If a warning does not appear on that official record, it does not enter the insurance underwriting process.

What affects your premium over time is documented driving behavior and how consistently you manage measurable risk.

How to Protect Your Insurance Rate

You protect your insurance rate by avoiding documented violations, preventing at fault accidents, maintaining strong credit where allowed, and using insurer approved discount programs that reward consistent, measurable safe driving behavior.

Insurance premiums respond to recorded risk. The most effective strategy is preventing chargeable events from entering your driving history in the first place.

Once a violation or accident is officially documented, underwriting models adjust pricing based on severity and frequency.

Safe driving habits reduce exposure to citations and collisions. Consistency matters more than short term correction.

Focus on the fundamentals:

- Follow posted speed limits

- Avoid phone use while driving

- Maintain safe following distance

- Obey traffic signals and stop signs

- Drive defensively in high traffic areas

These actions lower the likelihood of violations that trigger premium increases.

Monitoring your record also protects your rate. Request your driving record annually through your state DMV and verify that all entries are accurate. Correcting errors early prevents improper surcharges at renewal.

Reviewing your policy each year strengthens cost control. Compare quotes from multiple insurers, reassess deductibles, and confirm eligibility for available discounts.

Additional protective measures include:

- Completing approved defensive driving courses

- Enrolling in telematics or usage based programs

- Maintaining stable credit where legally permitted

Rate stability depends on preventing documented violations and maintaining accurate records. Consistent safe driving and regular policy review reduce the risk of premium increases.

Protect your insurance rate by reviewing your driving record and speaking with a reliable insurance agent about available discounts and risk reduction options.

Conclusion

A police warning alone does not raise your insurance because insurers adjust premiums based on documented violations and convictions. If there is no ticket, no court record, and no entry on your driving record, your rate remains unchanged.

Insurance companies price risk using official, court finalized data. If an event does not appear on your motor vehicle record, it does not enter the underwriting system and cannot trigger a surcharge.

Focus on what actually affects premiums: convictions, at fault accidents, license actions, and claim history. Monitor your record regularly and prevent chargeable violations to keep rates stable over time.