Auto insurance and vehicle ownership are legally connected. Financial responsibility laws apply the moment a vehicle is operated on public roads. In almost every state, drivers must carry liability coverage or provide proof of financial responsibility.

According to the Insurance Information Institute, every state except New Hampshire has compulsory auto insurance requirements.

State agencies monitor insurance compliance through registration systems, lender reporting, and electronic verification databases. These systems are designed to prevent uninsured vehicles from circulating on public roads.

Financing agreements and lease contracts also include insurance conditions that must be satisfied before a vehicle can be released.

The timing of insurance activation often creates confusion during a purchase. Ownership transfer, registration processing, lender approval, and vehicle delivery each involve insurance verification at different stages.

A misunderstanding about when coverage must begin can delay a transaction or create legal exposure. Knowing how these requirements connect to the buying process prevents penalties, protects personal assets, and ensures compliance from the first mile driven.

Do I Need Insurance Before I Buy a Car?

You do not need an active auto insurance policy before selecting or negotiating a car, but coverage must be arranged and active before the vehicle is legally driven, financed, or registered in your name under state financial responsibility laws.

Insurance is not required to visit a dealership, compare vehicles, or negotiate pricing. The legal requirement is tied to operation and ownership, not shopping activity. The obligation begins when the vehicle will be driven on public roads or formally transferred into your name.

Once you take possession and intend to operate the vehicle, coverage must already be active. The policy must meet state minimum liability limits and identify the specific vehicle by its vehicle identification number. Without this, the vehicle cannot legally be driven.

Dealerships and lenders verify insurance before releasing the vehicle. This applies whether you are paying cash or financing the purchase. If financing is involved, additional coverage is required beyond basic liability.

Financed vehicles usually require:

- State minimum liability coverage

- Collision coverage

- Comprehensive coverage

- Deductible limits approved by the lender

These protections secure the lender’s financial interest in the vehicle. Without proof that these coverages are active, the lender will not fund the loan and the dealership will not release the car.

Timing is critical. The effective date of the policy must match or precede the moment you take possession. A policy scheduled to begin the following day does not satisfy the requirement if you plan to drive immediately.

Most insurers can activate coverage the same day. Buyers often contact their insurance company from the dealership to add the new vehicle to an existing policy or start a new one. The insurer will request specific information before binding coverage.

You should be prepared to provide:

- Vehicle identification number

- Purchase date

- Lienholder information if financing

- Selected coverage limits and deductibles

Once coverage is bound, a digital insurance card is typically issued immediately. This serves as proof for the dealership and lender.

Private sales follow the same insurance rules. The seller’s policy does not transfer with the vehicle. Coverage under the seller’s insurance generally ends once ownership changes.

Before completing a private purchase, you must:

- Contact your insurer

- Add the vehicle to your policy

- Confirm the effective date and time

- Obtain proof of coverage

Driving away without activating your own insurance exposes you to full financial responsibility for any accident.

Some policies include automatic coverage for newly acquired vehicles. These provisions are limited and require timely notification to the insurer. Coverage levels may default to those carried on an existing vehicle. Confirming the exact terms with your insurer prevents gaps in protection.

Insurance activation is a legal checkpoint in the buying process. It affects vehicle release, loan approval, registration, and lawful operation.

Coverage must be active before the first mile is driven, which makes it essential to understand exactly when insurance must be active in the purchase timeline.

When Auto Insurance Must Be Active

Auto insurance must begin before a newly acquired vehicle is operated, transferred into your name, financed, or leased. The policy must list the vehicle, meet state liability limits, and be effective at the exact time possession changes or road use begins.

The activation of auto insurance is tied to legal control and physical possession of the vehicle. The critical moment is not payment or contract signing alone. It is the point at which the buyer has authority to operate the vehicle and intends to place it on public roads.

Coverage must be in effect at the precise time the vehicle becomes road bound. Insurance companies allow policies to be scheduled with specific effective dates and times. The start time must match the pickup time. A delay of even a few hours creates a coverage gap.

Different transaction structures change when activation must occur. The table below outlines when insurance must legally begin based on acquisition method.

| Acquisition Method | Activation Trigger | Coverage Start Requirement |

| Cash purchase at dealer | Physical possession | Before vehicle exits premises |

| Private party purchase | Title transfer | Before vehicle enters roadway |

| Loan financing | Loan funding approval | Before lender finalizes funding |

| Vehicle lease | Lease execution and delivery | Before keys are released |

Insurance must reflect the exact vehicle being acquired. The policy must include the correct vehicle identification number, make, model, and year. Errors in vehicle details can invalidate proof at the point of verification.

Leased and financed vehicles add contractual insurance standards beyond state liability minimums. Financial institutions typically require broader protection.

Standard contractual requirements often include:

- Full replacement value protection

- Comprehensive coverage for non collision loss

- Collision coverage for accident damage

- Maximum deductible thresholds defined in agreement

Failure to maintain these standards can result in forced insurance placement by the lender. Forced policies protect only the lender’s interest and increase monthly costs.

Registration systems in most states electronically confirm insurance status. Insurance data is cross checked with state databases before registration or plate issuance is completed. Delays in database updates can interrupt the process if activation is not timed correctly.

Before finalizing possession, confirm the following operational checkpoints:

- Exact policy effective date and time

- Accurate vehicle identification number entry

- Coverage limits aligned with legal requirements

- Additional protections aligned with contract terms

Insurance activation must be treated as a synchronized legal event. Payment processing, policy issuance, lender approval, and vehicle delivery must align precisely. Any gap between ownership transfer and policy activation exposes the buyer to immediate liability.

The requirement is triggered by control and use. The moment the vehicle is capable of lawful road operation under your authority is the moment insurance must already be in force, and that timing plays out differently depending on whether you are buying from a dealer or a private seller.

Auto Insurance for Dealer vs Private Sales

Auto insurance must be active before driving away from a dealer or a private seller. Dealers verify coverage before releasing the car and lenders add coverage conditions, while private sales require the buyer to activate and confirm insurance independently.

The source of purchase changes the process, documentation flow, and verification steps. The legal requirement for active auto insurance remains the same. What differs is who verifies coverage and when confirmation must occur.

Dealer Purchase

Dealers require proof of auto insurance before completing final paperwork and releasing the vehicle. The policy must list the vehicle identification number and meet state minimum liability limits. If financing is involved, lenders require additional protection.

Dealership requirements usually include:

- Active liability coverage meeting state limits

- Vehicle identification number listed on the policy

- Collision and comprehensive coverage if financed

- Digital or printed proof of insurance

Dealers often verify insurance electronically before releasing keys. Lenders also confirm coverage before funding the loan. Without verified insurance, the vehicle cannot leave the lot.

Private Seller Purchase

Private sales require the buyer to manage insurance independently. The seller’s insurance does not transfer after ownership changes. Once the title is signed over, the buyer assumes responsibility.

The flowchart above shows that before completing payment, the buyer must contact their insurer, add the vehicle to the policy, confirm the effective date and time of coverage, and obtain digital or printed proof of insurance to ensure the vehicle is properly insured at pickup.

Insurance must be active before entering public roads. Driving without activating your own policy places full financial responsibility on you for any damages or injuries, and financing a vehicle adds another layer of insurance requirements that go beyond basic state liability limits.

Auto Insurance Requirements for Financed Vehicles

Financing a vehicle increases insurance requirements beyond state minimum liability coverage. Lenders require collision and comprehensive protection, set deductible limits, and may impose force placed insurance if required coverage is not maintained.

Financing changes insurance from a legal requirement to a contractual obligation. When a lender provides funds to purchase a vehicle, the lender holds a financial interest in that vehicle. Insurance must protect both the driver’s liability exposure and the lender’s asset.

State law requires liability insurance. Loan agreements require broader protection. These requirements are written into the finance contract and must be satisfied before loan funding is completed.

Most lenders require the following coverage:

- Liability coverage meeting or exceeding state minimum limits

- Collision coverage for accident related damage

- Comprehensive coverage for theft, fire, vandalism, and weather damage

- Deductible limits that fall within lender approved thresholds

Liability insurance protects other drivers and property. Collision and comprehensive protect the vehicle itself. Without physical damage coverage, the lender’s collateral is exposed to loss.

Deductibles are often restricted. Many lenders require maximum deductibles, commonly between five hundred and one thousand dollars. Higher deductibles reduce premiums but increase lender risk, which is why limits are imposed.

Insurance verification is required before loan funding. The policy must list:

- The financed vehicle by vehicle identification number

- The lender as lienholder

- Coverage limits that meet contractual terms

- An effective date aligned with possession

If any element is missing, funding is delayed.

Failure to maintain required coverage during the loan term creates serious consequences. Lenders monitor insurance status through electronic reporting systems. If coverage lapses, the lender issues a notice requiring proof of reinstatement.

If the borrower does not restore coverage, the lender can purchase force placed insurance. According to the Consumer Financial Protection (CFPB) Bureau, lenders may add force placed insurance when required coverage is not maintained.

Force placed insurance carries several characteristics:

- Significantly higher premiums

- Limited coverage focused on the lender’s interest

- No liability protection for the driver

- Charges added directly to the loan balance

This type of policy protects only the vehicle’s value for the lender. It does not protect the borrower from liability claims after an accident.

Leased vehicles operate under similar but often stricter standards. Leasing companies commonly require higher liability limits than state minimums. They also mandate full collision and comprehensive coverage with defined deductible caps. Proof must be provided before vehicle delivery.

Failure to comply with insurance requirements in a lease agreement can result in:

- Lease violations

- Additional fees

- Mandatory insurance placement

- Contract termination

Financing extends insurance obligations beyond the initial purchase. Coverage must remain continuous for the entire loan or lease term. Any lapse exposes both legal and contractual consequences.

Insurance becomes a binding financial condition tied directly to vehicle ownership under a lending agreement, which makes it important to understand how temporary coverage and grace periods actually work.

Temporary Insurance and Grace Periods of Auto Insurance

Temporary coverage of auto insurance may extend to a newly purchased vehicle for a limited time under an existing policy, but terms vary by insurer. Grace periods require notification within a set timeframe, and coverage must be confirmed before driving.

Temporary auto insurance coverage applies when an existing policy includes automatic protection for newly acquired vehicles. This provision allows short term coverage before the vehicle is formally added to the policy. The duration and scope depend entirely on the policy contract.

State insurance regulators confirm that coverage terms vary by policy and insurer. The National Association of Insurance Commissioners explains that auto insurance provisions, including newly acquired vehicle clauses, differ by state and carrier.

Automatic coverage is not universal. It only applies if written into the policy. Even when included, it operates under strict conditions.

Common automatic coverage provisions include:

- 7 to 30 day temporary coverage window

- Coverage equal to the broadest protection on an existing vehicle

- Mandatory notification to the insurer within a specific timeframe

- Immediate cancellation if notification is not made

If notification is not provided within the required period, coverage may be denied. The vehicle may then be treated as uninsured from the moment it was acquired.

Below is a clearer breakdown of how temporary coverage typically works:

| Provision Element | Typical Rule | Risk if Ignored |

| Coverage Duration | 7 to 30 days from acquisition | Claim denial after deadline |

| Coverage Level | Same as existing insured vehicle | No automatic upgrade in limits |

| Notification Requirement | Must notify insurer within timeframe | Coverage may be voided |

| VIN Listing | Vehicle must be formally added | Registration or claim delays |

Automatic coverage does not replace updating the policy. The vehicle identification number must be added, and the insurer must confirm the effective date.

Temporary insurance binders are another option. A binder is written confirmation that coverage is active before the full policy is issued. It is often used when immediate proof is required.

Binders are commonly used when:

- Purchasing from a private seller

- Switching insurers at the time of purchase

- Providing proof to a lender

- Registering the vehicle immediately

A binder confirms coverage limits, deductibles, and effective time. It functions as legal proof during its valid period.

Grace periods are conditional and time sensitive. Written confirmation prevents misunderstandings and ensures continuous auto insurance coverage from the moment ownership begins, and that continuous coverage becomes critical when meeting state registration and insurance proof requirements.

State Registration and Insurance Proof

Vehicle registration requires active auto insurance. State motor vehicle agencies verify coverage electronically before issuing plates or finalizing registration, and auto insurance lapses can trigger suspension, fines, or vehicle impoundment.

State motor vehicle agencies connect vehicle registration directly to auto insurance compliance. Registration authorizes legal road use. Auto insurance satisfies financial responsibility laws. Both must remain active at the same time.

Most states rely on electronic auto insurance verification systems. Insurers transmit policy data to state databases. When registration is processed, the system confirms whether valid auto liability coverage exists.

Registration approval generally requires:

- Active auto liability insurance meeting state minimum limits

- Auto insurance policy correctly linked to the vehicle identification number

- Continuous auto insurance coverage without interruption

- Successful electronic auto insurance verification through state systems

If auto insurance coverage cannot be verified, registration may be denied or suspended.

State Examples of Auto Insurance Registration Laws

Many states explicitly tie auto insurance to vehicle registration status.

- California requires active auto insurance before registration is finalized

- Texas requires auto insurance proof before issuing license plates

- Florida requires minimum auto liability insurance before vehicle operation

The Florida Department of Highway Safety and Motor Vehicles confirms that uninsured drivers face suspension and reinstatement penalties.

Penalties for Auto Insurance Lapse

When an auto insurance policy is canceled or expires, insurers report the lapse to state systems. Enforcement may begin automatically.

Common penalties include:

- Monetary fines for lack of auto insurance

- Driver license suspension

- Vehicle registration suspension

- Vehicle impoundment

- Reinstatement and administrative fees

In many states, registration suspension occurs even if the vehicle is not being driven. Continuous auto insurance coverage is required to restore registration.

How States Verify Auto Insurance Coverage

Auto insurance verification occurs during:

- Initial vehicle registration

- License plate issuance

- Registration renewal

- Traffic stops and enforcement checks

Digital or printed auto insurance cards may be requested, but electronic database confirmation determines compliance.

Vehicle registration and auto insurance operate as connected legal requirements. Continuous auto insurance coverage preserves both legal road use and registration validity, and preparing that coverage before completing a vehicle purchase prevents delays and compliance issues at pickup.

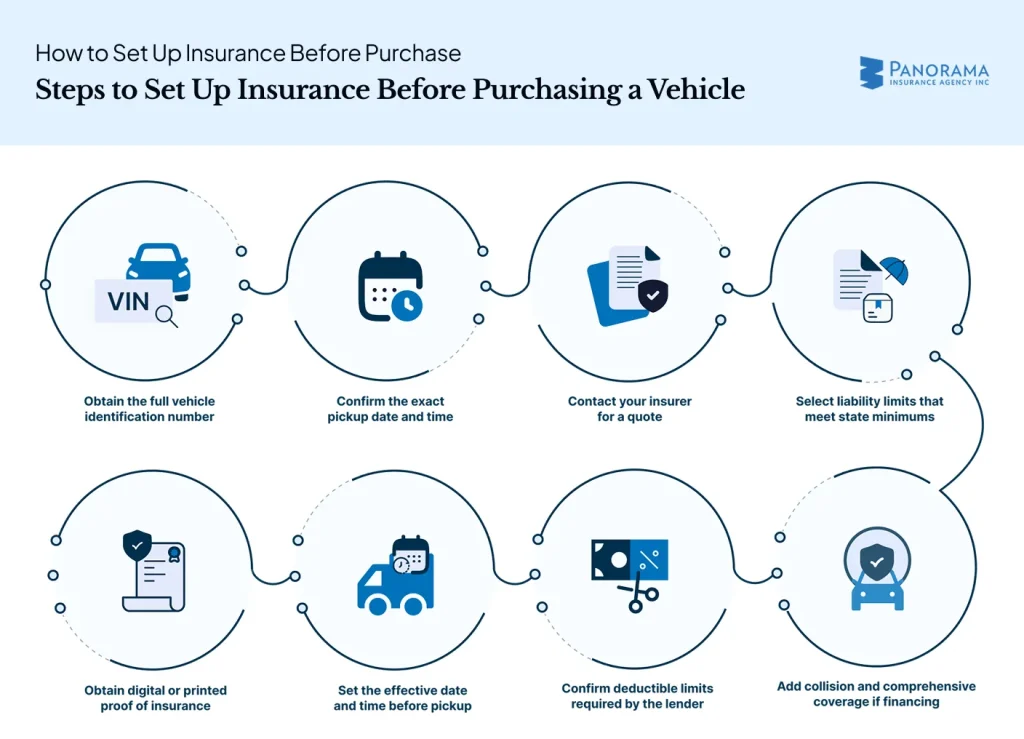

How to Set Up Insurance Before Purchase

Auto insurance must be arranged and activated before taking possession of a vehicle. The policy must list the correct VIN, meet state liability limits, include lender required coverage if applicable, and be effective before the vehicle is driven.

Auto insurance setup should begin once you select the vehicle you intend to buy. Activation timing must match the moment possession transfers. Coverage details must align with state law and, if financing, lender requirements.

Before completing the purchase, prepare the required information and confirm activation.

The flowchart above outlines the steps to set up insurance before an auto purchase, including obtaining the vehicle identification number, confirming the pickup date, contacting your insurer for a quote, selecting proper liability and full coverage if required, setting the effective date, and securing proof of insurance before pickup.

The vehicle identification number must be entered correctly on the policy. Liability limits must satisfy financial responsibility laws. If the vehicle is financed or leased, the lender must be listed as lienholder on the policy.

Insurers can bind coverage the same day. Effective time should be set before you take possession. A policy that begins after pickup creates a coverage gap.

Dealerships and lenders typically verify:

- Policy number

- Effective date and time

- Coverage types and limits

- Lienholder listing if applicable

Digital insurance cards are widely accepted and usually issued immediately after binding.

Coordinating coverage in advance prevents delays at pickup, funding interruptions, and registration issues. With activation completed before possession, you can ensure continuous auto insurance protection from the first mile driven.

Conclusion

Auto insurance does not need to exist before shopping for a vehicle, but it must be active before you drive, register, lease, or finance the car under state financial responsibility laws that apply the moment the vehicle enters public roads.

Auto insurance functions as a legal and contractual safeguard tied directly to vehicle ownership. State agencies, lenders, and leasing companies each rely on verified coverage before completing their respective processes.

Insurance status is often confirmed electronically, and inconsistencies can halt transactions immediately.

Maintaining accurate and uninterrupted coverage protects against more than accident costs. It prevents administrative penalties, funding interruptions, registration holds, and forced insurance placement.

Reviewing policy details before pickup ensures compliance with liability limits, contractual terms, and identification requirements.

Proper timing, documented confirmation, and continuous monitoring of policy status keep ownership compliant from the start. Clear preparation removes uncertainty and supports lawful operation without interruption.